Non-Concessional Contributions

Non-Concessional Contributions

Non-concessional contributions are generally personal contributions for which you do not claim a tax deduction.

As with Concessional Contributions, there are also Non-Concessional Contributions Caps (NCCC) for each financial year. For the current 2010-11 year the NCCC amount is $150k. From 1 July 2009 the NCCC is 6x the concessional contributions cap of $25k.

This time, there is no transitional cap for non-concessional contributions, however there is a ‘bring-forward’ provision which allows persons under 65 during a financial year to bring forward 2 years’ entitlements thereby giving access to a total of 3 years worth of NCCCs .

Essentially; in 2010-11 an individual may make up to $450k of non-concessional contributions, (being 3x $150k.) The individual then cannot contribute more non-concessional contributions until after 1 July 2013.

The Government Co-contribution

In 2003 the Australian Government passed legislation regarding Non-Concessional Contributions. This was introduced as an incentive for low to middle income earners to start actively saving more for retirement. The government initially matched dollar for dollar Non-Concessional Contributions made by eligible individuals.

This amount was then increased to 150% for the 2005 – 2009 financial years. The rate has now been reduced back to 100% from the 2009-10 financial year and beyond, up to a maximum of $1k.

The government co-contribution is not subject to income tax when received by a super fund doesn’t make up assessable income of the fund. It is classified as “preserved.”

Who is eligible to contribute to Super?

Any person under 65 may contribute to super regardless of employment status.

Personal deductible and non-concessional contributions may also be made persons aged 65 – 74 provided they work at least 40 hours in a period of not more than 30 consecutive days in the year.

A person aged 75+ is not able to make personal contributions to superannuation. An employer contribution for an employee over 75 is only deductible if the employer is required to make the contribution by an industrial award.

In addition, from 1 July 2007 provisions have been introduced that require a fund to return personal contributions where a member has not provided their Tax File Number (TFN.) These provisions were brought in more effectively administer the super system, in particular – the super caps. Once a super fund is aware that it has received a personal contribution from a member for whom they have no recorded TFN, they have 30 days to return the contribution. The contribution does not have to be returned if a TFN is provided for the member within 30 days.

Summing Up!

Making contributions to superannuation isn’t always a simple thing. The contribution caps are strict and if they’re exceeded, the penalties can be severe – excess contributions tax can apply and the consequences are very expensive!

Latest News / Blog Post

Posted on February 21, 2011

Understanding Non-Concessional Super Contributions

Tagged With: Concessional | Contributions | Non-Concessional | Retirement | Savings | SGC | Super Guarantee | Superannuation

RECENT POSTS

CATEGORIES

Previous Articles

February 14, 2024

February 14, 2024

Life Insurance: The Ultimate Gift of Love this Valentine’s Day

It's Valentine's Day. Love is in the air, and some of us are searching for that perfect gift to express our affection for those closest to us. And despite a grisly past, this day has come to be known for lovers... So just what is the ultimate gift of love this Valentine's Day? While chocolates and flowers are lovely, this...

May 8, 2023

May 8, 2023

Should I Pay off my HECS Debt?

Should I pay off my HECS debt early? Many are asking in light of the coming large CPI increase.

March 20, 2023

March 20, 2023

Global Banking System Volatility

Silicon Valley Bank Failure! Market volatility has been elevated over the past week driven by the failure of the Silicon Valley Bank (SVB). Global banking system volatility is on the rise! The unfolding situation in the US could be seen by some as having echoes of the Global Financial Crisis (GFC) from 2008. This, combined with recent falls in Credit Suisse...

September 19, 2022

September 19, 2022

Time is running out!

Time is running out to apply for a Director Identification Number (director ID) You may have heard about the new rules which require directors of Australian companies to obtain a Director Identification Number (director ID). It is a unique 15-digit identifier that directors apply for once and keep forever. The following provides some useful further information. As a director of...

June 28, 2022

June 28, 2022

Staying passive is being active

Staying the Course Heightened global markets volatility can easily trigger kneejerk reactions by panicked investors. Widespread selling, triggered by the Russia-Ukraine crisis, has been behind recent big swings on global financial markets. This includes stock markets, commodities and currency markets. As serious as the current events are, heightened market volatility is nothing new. The onset of the COVID-19 pandemic also...

June 27, 2022

June 27, 2022

Market Update – June 2022

Volatility is Normal The volatility that we've seen over the last six months, while significant, is not an unusual occurrence for a normal and healthy functioning market. Heightened volatility is an uncomfortable experience in the short- term. Equity markets and some parts of the bond markets will continue to be an important contributor to overall long-term returns. We appreciate that...

June 14, 2022

June 14, 2022

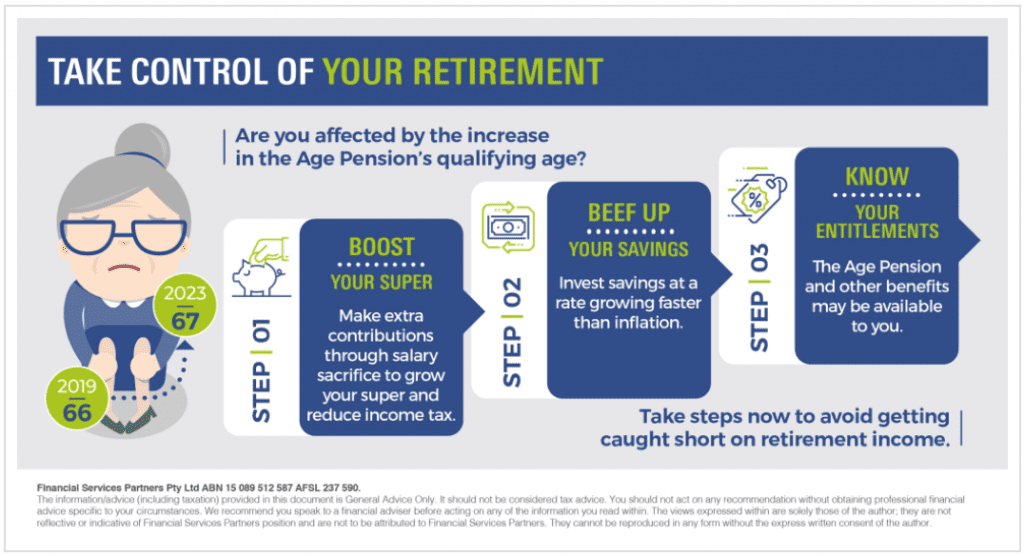

Take Control of your Retirement

Are you approaching retirement? Chances are the funding of your lifestyle in retirement may be on your mind! Take steps now to avoid getting caught short on retirement income and live the retirement lifestyle you want. It's time to take control of your retirement. The qualifying age is increasing by six months every two years until it reaches 67 in...

February 28, 2022

February 28, 2022

Russia Ukraine Update

Russia Ukraine Event Update On 21 February, Russia asserted its view on the independence of the Donetsk People’s Republic and the Luhansk People’s Republic. Russia began mobilising troops to conduct peacekeeping operations. This was a violation of Ukraine’s sovereignty and independence, the Minsk agreement, and has been widely denounced by the West. Subsequently, Russia instigated military strikes on Ukraine and...

February 25, 2022

February 25, 2022

Russia Ukraine Concerns and your Finances

Worried about the impact of Russian Ukraine concerns and your finances? Please reach out directly to the Wealth Planning Partners team if you want to discuss your personal financial plan. So, a little perspective on the Ukraine and Russian situation. This geopolitical event is concerning on practically every level. And there are a wide range of potential outcomes and scenarios....

December 4, 2020

December 4, 2020

Dreaming about money? What does it mean?

Do you dream about money? Daydream even? When you have dreams about money, it can be a bit of an interesting view into what your subconscious is thinking about when it comes to the topic of money or finances. Your dreams can influence your decisions, so it's a good idea to delve deeper into what you're dreaming about. Are you...

November 2, 2020

November 2, 2020

Tenants in Common vs Joint Tenants

What is ‘Tenancy In Common' 1. "Tenancy in common" allows two or more people to be owners in a property. Each owner has the authority to will their share to anyone on death. 2. "Tenancy in common" is different as the transfer of the property in the event of death differs. In joint tenancy, the title of the property automatically...

October 28, 2020

October 28, 2020

Are you a slave to money?

From a young age we are taught… GOOD GRADE = GOOD UNIVERSITY = GOOD JOB = GOOD MONEY Teenagers are believing that this is the only route to lead a success. It’s a cycle, churning throughout time – being handed down from generation to generation, merely reciting what they heard from parents and teachers in the early stages of their...

October 27, 2020

October 27, 2020

The skills advisors need to handle suspected financial abuse

Gold Coast based financial adviser Amanda Cassar says " advisers need skills to handle financial abuse." Could you confidently recognise a warning sign of financial abuse? Unfortunately, financial abuse is becoming increasingly more visible on a global scale. It does not discriminate. This type of abuse can occur irrespective of someone's economic status, level of education, race, gender or ethnicity. ...

October 26, 2020

October 26, 2020

How do I save for a house after being hit by COVID?

How do you save for a house after being hit by the fallout from COVID? Have you been struggling financially with the COVID-19 pandemic? Has the global pandemic affected your income? How's you financial stress level, not only in your household, but your overall mental health? If so, how can you get back on track after being hit by CoVid?...

October 22, 2020

October 22, 2020

Are we teaching our kids to manage money?

Are you teaching your kids how to manage their money? Teaching our children about money is vital. Do you know how to teach your kids to manage money? When interviewing for her book “Financial Secrets Revealed,” Amanda Cassar found most of us haven’t been taught how to manage money by their parents. Are you self taught? And what do you...

October 12, 2020

October 12, 2020

Get Ready for Storm Season, Queensland!

Get ready for storm season! The Queensland Government want everyone to Get Ready for disaster season. Use the 3 Step "Get Ready" Plan. Prepare your household this storm season by completing these 3 simple steps: Have a plan Firstly, ensure your family is equipped with an emergency and evacuation plan. Make sure everyone knows what to do in a disaster. Team-up...

October 7, 2020

October 7, 2020

Federal Budget Update 2020 – How the Budget may affect families

How does Federal Budget 2020 impact Families?

September 28, 2020

September 28, 2020

How to take control of your retirement

Are you affected by the increase in the Age Pension’s qualifying age? Take steps now to avoid getting caught short on retirement income. The minimum age to qualify for the Age Pension has started going up. For those born on or after 1 July 1952, the qualifying age increases by six months every two years until it reaches 67 in...

September 28, 2020

September 28, 2020

How do I invest my money?

So, how do you invest your money? When deciding how to go about investing those hard earned dollars, you need to decide whether you'll: do it yourself, or pay a financial advisor to do it for you Both options have their pros and cons. However, you can - of course, do a bit of both. Buy, sell or invest yourself...

Head Office

P.O Box 3592, Burleigh Town, QLD, 4220

Contact Us

Phone: 07 5593 0855

Email: info@wealthplanningpartners.com.au

Office Hours:

9am - 5pm Monday to Thursday

9am - 3pm Friday

(Other appointment times by request)

![]()

Registration

WPP Licensee Services Pty Ltd

P.O Box 3592, Burleigh Town, QLD, 4220

Robina, QLD, 4226

AFSL No. 530393

ABN# 76 649 079 998

Copyright © 2023 Wealth Planning Partners Pty Ltd | All Rights Reserved | Website designed by Xenex Media